/

Send us an emailinfo@mvmotion.com

© 2026 MV Motion All rights reserved.

All Research / Automotive & EVs, Robotaxis & Autonomy, +1 more

May issue of our newsletter highlights stories on multiple mass robotaxi deployments, new partnerships, acquisitions, regulatory developments, as well as interesting humanoid robot unveilings. RobotaxiMap.com has recorded a modest number of new locations, including Tesla launches across Texas and Waymo's intention to launch in Oregon.

The newsflow in robotaxis and humanoid robots can be overwhelming. Each month, Martin Viecha and the MV Motion team summarize the most important news stories, share our perspective, and comment on the latest deployments on RobotaxiMap.com. Stay on top of the industry in 5 minutes - or dig deeper, if you prefer!

This month, we present you with 7 exciting news story picks and 2 Robotaxi Map deployment updates, although the biggest update on the RobotaxiMap.com has been the addition of Fleet Sizes and Ride Counts. Make sure to check them out!

Robotaxis are entering a scaling era as companies shift from pilots toward industrialized deployment targets. Tesla’s Cybercab is moving towards commencing mass production, WeRide has outlined ambitions for 200,000 robotaxis, CaoCao and Geely are targeting 100,000 custom-designed robotaxi vehicles, and Rivian has referenced a 50,000-vehicle robotaxi program with Uber. Together, these targets point to a transition from city-level experimentation to large fleet manufacturing, platform integration, and supply-chain readiness for autonomy at commercial scale.

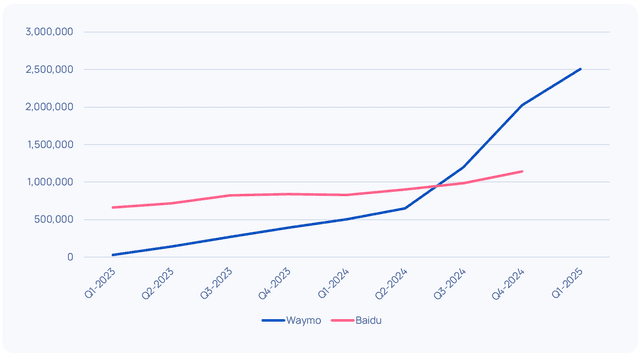

There are fewer than 10,000 robotaxis in operation globally today, but we are already hearing about >100k robotaxis just for a single company. In reality, deployment is not bound by ability to produce robotaxi vehicles. It is bound by a) legislation; b) lead time to build mass parking & charging locations; c) software that actually works in rain or snow or any other difficult weather conditions. Thus far, Waymo has been generally far more cautious about delivering growth while beating their own estimates. To put things into perspective, Waymo is expecting to achieve a fleet size of ~6,000 by the end of 2026 (perhaps they get to 7-8k), while other companies with less capable software are talking about 100,000s of robotaxis. It's hard to take such announcements too literally. Furthermore, China's suspension of robotaxi license issuance in the wake of Baidu's Wuhan outage highlights how easily such ambitions can be set back despite promising development thus far.

Hertz launched Oro Mobility as a fleet-management affiliate aimed at supporting commercially operated vehicle fleets. Under its Uber partnership, Oro will handle day-to-day operations for Uber’s planned robotaxi fleet, including charging, maintenance, repairs, cleaning, and depot staffing. The vehicles are expected to be Lucid models equipped with Nuro autonomous-driving technology, with initial services planned for the San Francisco Bay Area later this year and possible expansion in 2027. The deal also extends Hertz’s role in driver-led Uber fleet operations.

We've been saying for a while that Robotaxi will in many ways resemble Airline industry. Maximizing utilization rate, pricing power, fleet reliability, lowering cost per mile, brand loyalty, etc - those are the topics that Airline industry likes to discuss, and the Robotaxi industry will be no different. Large fleet operation will require heavy staffing overnight for maintenance, repairs and cleaning. The most important cost item in running a robotaxi fleet is the cost of underutilization. Cost of a robotaxi vehicle itself is negligibly small (in terms of cost per mile) compared to cost of underutilization. It's good to see that companies are starting to focus on this critical cost item.

Tesla’s supervised FSD achieved its first European regulatory approval in the Netherlands. Following more than 18 months of testing and validation with Dutch authorities (and over 1.6M km of testing), Tesla's FSD software is on the cusp of getting approved. The approval allows deployment on public roads under driver supervision and represents the first authorization of Tesla’s system within the EU framework. Dutch regulators have initiated a process to notify the European Commission, which could enable broader EU-wide approval. Parallel testing programs continue in markets such as Spain, where Tesla has accumulated ~80,000 km of incident-free validation driving. Tesla has also reported that within the first month, Tesla owners in the Netherlands have driven over 10M km on FSD.

In the US, I've been using FSD city streets on my Tesla for over 5 years every day. At that time, an intersection done right (which was rare) felt like magic. By Oct-2025, with the release of FSD V14, the self-driving experience became so superior, I essentially stopped driving manually altogether. While Tesla owners have now driven nearly 10 billion miles using the FSD software, that wasn't convincing enough. It took this level of software advancement (FSD V14) as well as 18 months of testing and validation by the local authorities for them to get close to final approval. The bottom line is, Europe is far more cautious when it comes to robotaxi-enabling technology than US or China. Outside of US and China, it seems that the Middle East and the UK will be the main "battlefields" between American and Chinese robotaxi companies.

Meta Platforms acquired humanoid robotics startup Assured Robot Intelligence (ARI) for an undisclosed amount, bringing its ~20 person team into Meta’s AI and Superintelligence Labs. ARI focuses on “physical AI” systems that allow robots to interpret human behavior, learn from real-world interaction, and execute tasks in dynamic environments. The acquisition follows Meta’s earlier exploration of physical AI, including internal humanoid initiatives, robotics hiring, and research into tactile sensing, control, and embodied intelligence systems.

Since Meta has spent quite some time working on VR, virtual worlds and World Models, entry into a Humanoid Robot space is kind of an expected move. If Meta is one of the first companies to solve world models (their JEPA project), its deployment of humanoid robots would be an obvious next step after solving World Models. So instead of just selling its World Model to other humanoid robot companies, Meta has probably decided to just keep the whole stack in house. While Meta's VR headsets became the #1 VR product globally, it's still a niche product. Other than the VR headsets, Meta's track record on hardware is not bad, but not outstanding. Creating the most profitable set of social media networks requires a vastly different skillset than designing and deploying a humanoid robot. Still, this is a one to watch.

Xiaomi reintroduced its humanoid robot program with new CyberOne updates after several years of limited visibility, signaling a renewed push into embodied AI. Recent demonstrations showed improved dexterity, including a redesigned tactile hand and sustained execution of repetitive factory tasks, alongside internal pilots in EV manufacturing with >90% task success rates. CyberOne has also been upgraded to a V2 iteration, capable of basic social interaction at public events. The re-emergence follows ecosystem investments across robotics components, perception, and control, with no disclosed timeline for commercial deployment.

While there are too many companies launching humanoid robots, Xiaomi is hard to ignore. Even as a rookie in the field, they have shaken the autos industry to the core, with many claiming that Xiaomi's SU7 might be the best car in the world right now. Xiaomi's humanoid robot effort should be taken seriously as the company leverages its expertise in precision automation while operating car production lines too. While we understand that useful humanoid robots are still far away, entry by a company that is this capable in both software and hardware should not go unnoticed.

Tesla’s first Semi rolled off its high-volume production line at Gigafactory Nevada, moving the electric truck program beyond pilot builds and early PepsiCo deliveries. The Nevada Semi factory is designed for up to 50,000 trucks annually, though Tesla has not disclosed 2026 delivery volumes and has indicated a gradual ramp. The milestone adds a second major vehicle production ramp alongside Cybercab, with Semi targeting commercial freight operators and requiring continued Megacharger infrastructure deployment.

While the very first Tesla Semi deliveries in Dec-2022 were already delayed by 3 years (mainly due to lack of battery cell supply), it took another 3.5 years for high-volume production to start. And now, following the reports of Aurora trucks running 1,000-mile drives from Fort Worth to Phoenix (exceeding the federal hours-of-service for a single driver), and the announcement of the Swedish IPO-bound autonomous freight company Einride to develop autonomous corridor in Texas, it is highly expected that Tesla Semi will want to join the race of Autonomous Semi trucks. Especially for a depot-to-depot operation, an electric, autonomous truck is such a no-brainer.

California’s new robotaxi rules add enforcement powers over driverless fleets, including notices for traffic violations, emergency-response requirements, and DMV authority to restrict fleet size, speed, geography, or weather conditions. Texas is moving from a largely permissive model to mandatory TxDMV authorization for commercial driverless passenger operations, enforceable from May 28, 2026. Operators must certify compliance with traffic laws, recording-device requirements, insurance, registration, minimal-risk capability, and emergency-response plans. Together, the rules formalize oversight in two major robotaxi markets without banning commercial deployment.

The bottom line is that both new legislations in California and Texas act to shape the rules mainly based on Waymo's performance, but don't act to actively restrict. There have been too many examples of police officers struggling to "move" a robotaxi away. So both legislation clarify how robotaxis should act in those situations and how to get access to a teleoperator quickly. We are not expecting robotaxi deployment to slow down in these two states by any means. To put things into context, San Francisco Bay Area has more robotaxis in operation than any other city in the world, while Waymo's DMV permit in California already covers ~70% of the state's population. California, Texas and Florida remain some of the most welcoming states when it comes to robotaxis.

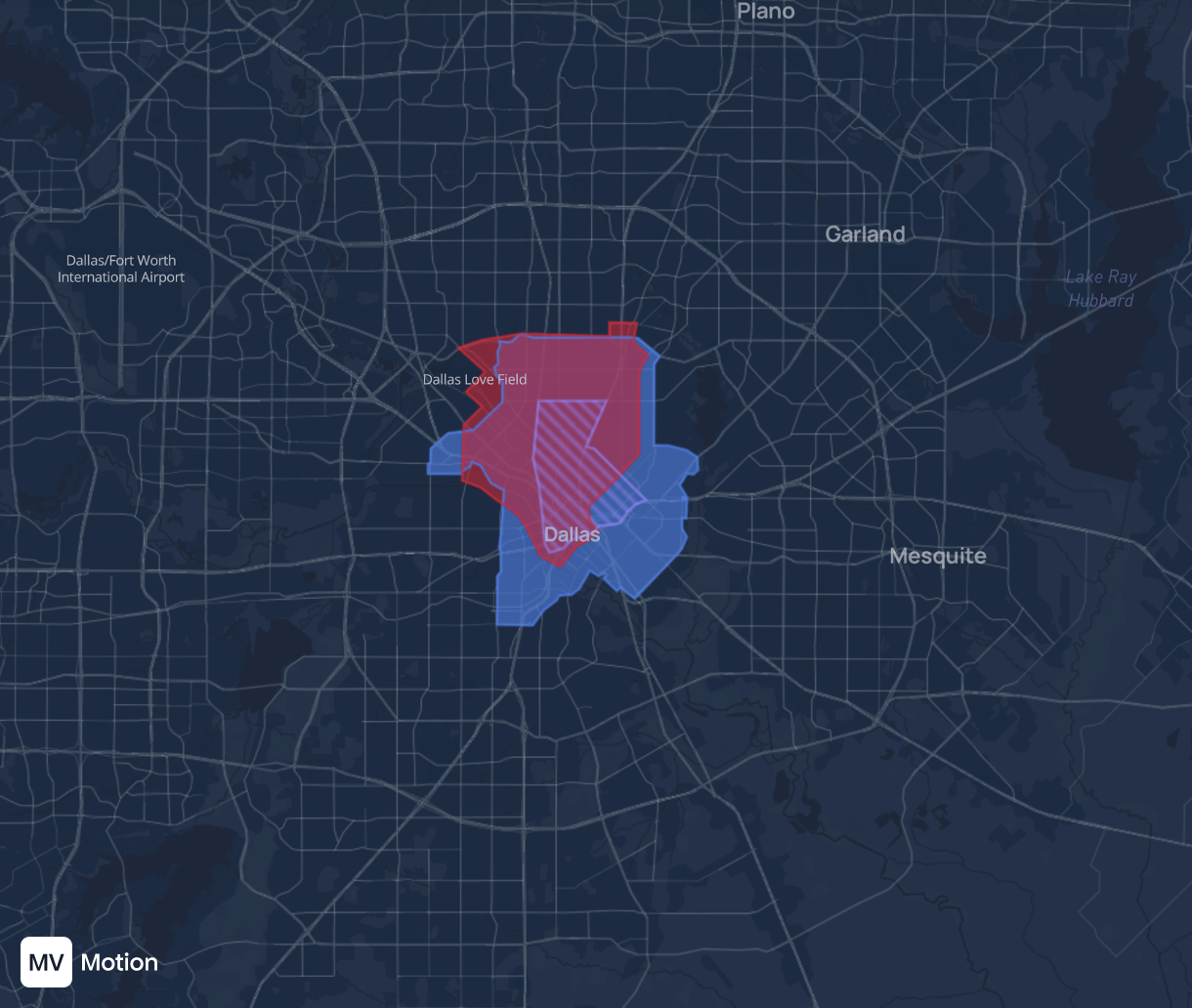

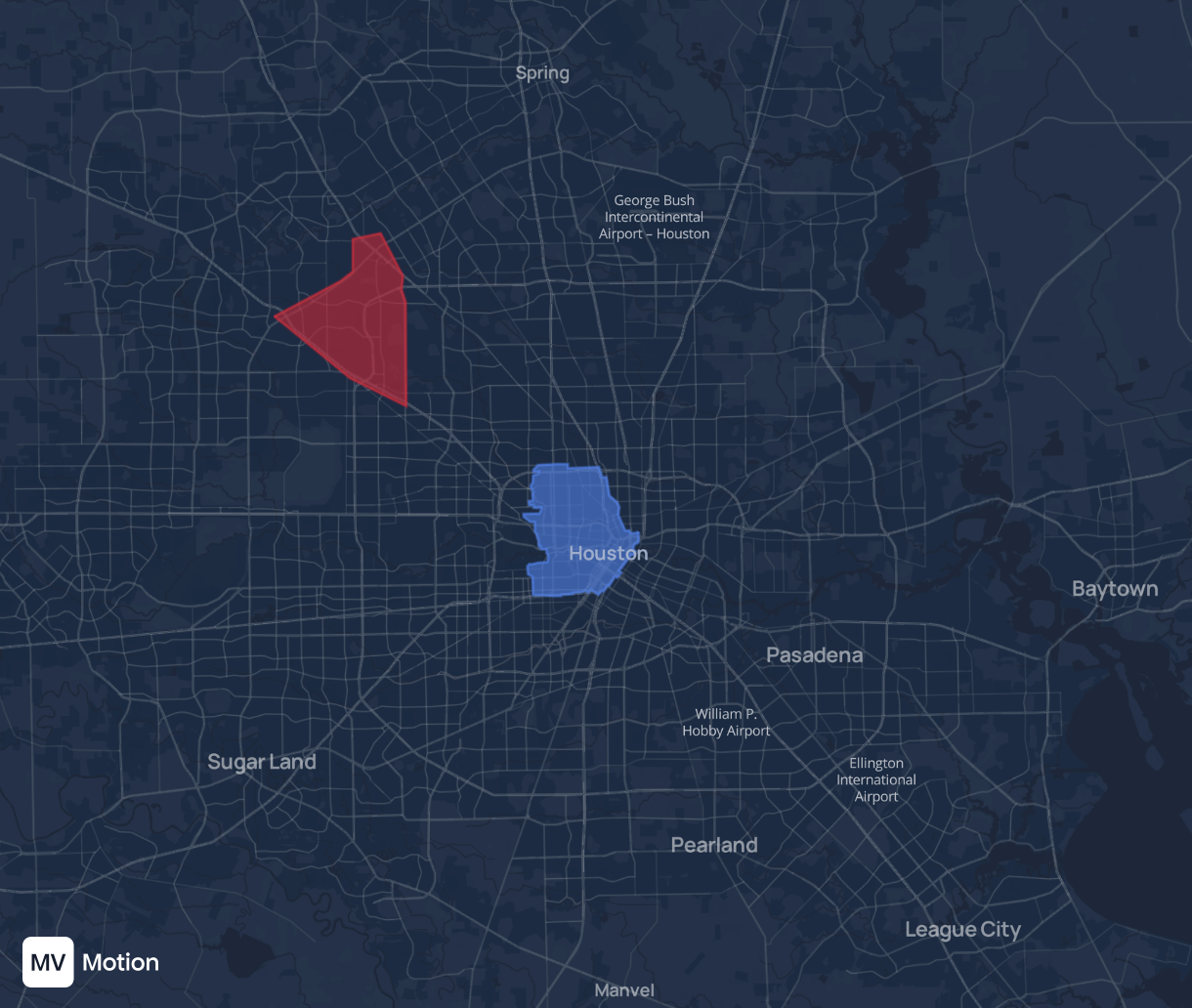

Tesla’s Dallas and Houston robotaxi launches mark its first Texas expansion beyond Austin, with official X videos showing Model Ys operating without in-car drivers or monitors, though fleet size and true unsupervised availability remain undisclosed. Like Austin, real driverless deployment is likely narrow, with reported geofences of roughly 25 to 30 square miles and very few cars. Dallas is the more strategic battleground: Tesla now overlaps with Waymo’s driverless service and Uber/Avride’s supervised robotaxi rollout, while Houston’s Tesla geofence appears notably separate from Waymo’s footprint.

Tesla vs Waymo and Avride in Dallas

Source: RobotaxiMap.com

Tesla vs Waymo in Houston

Source: RobotaxiMap.com

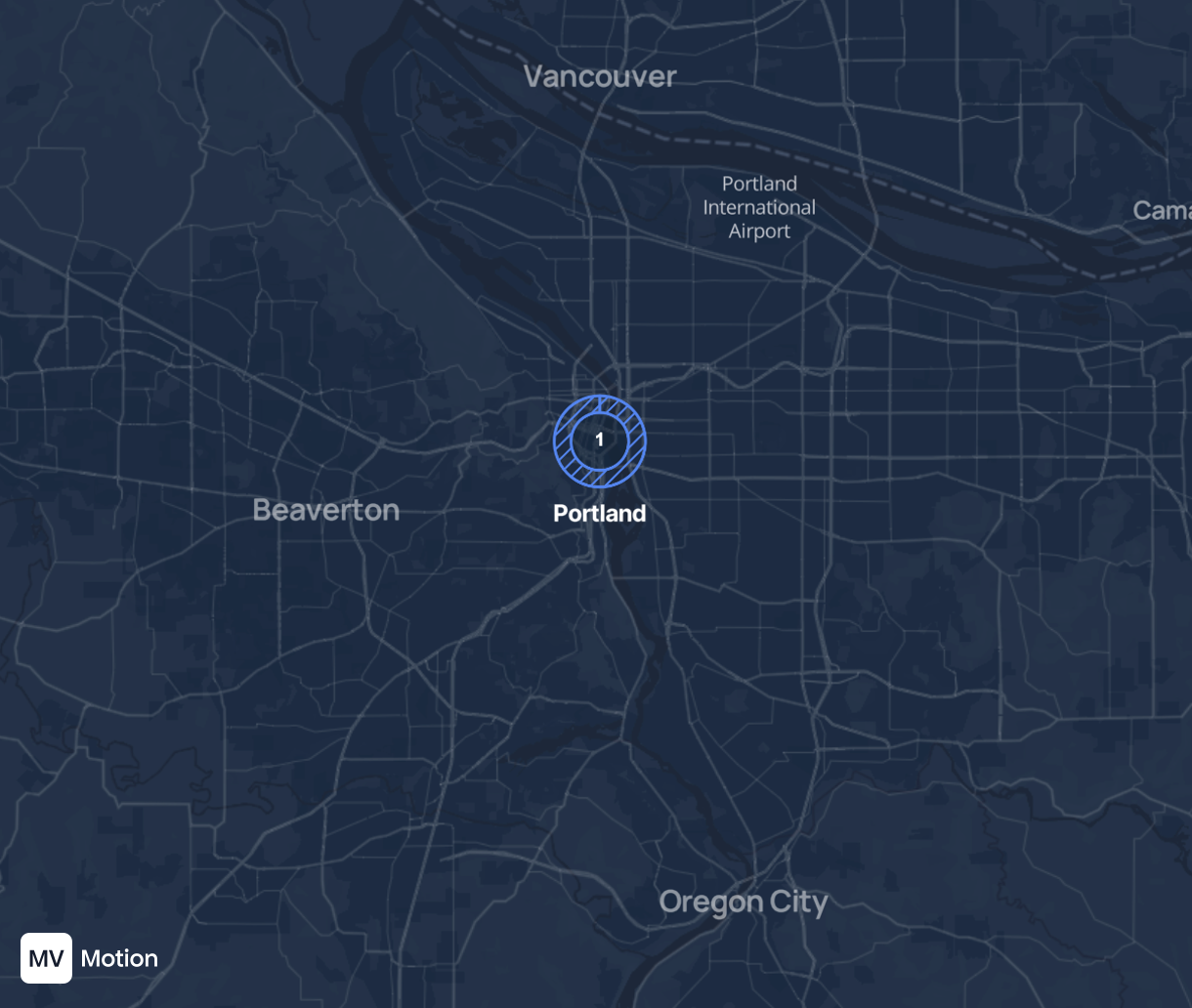

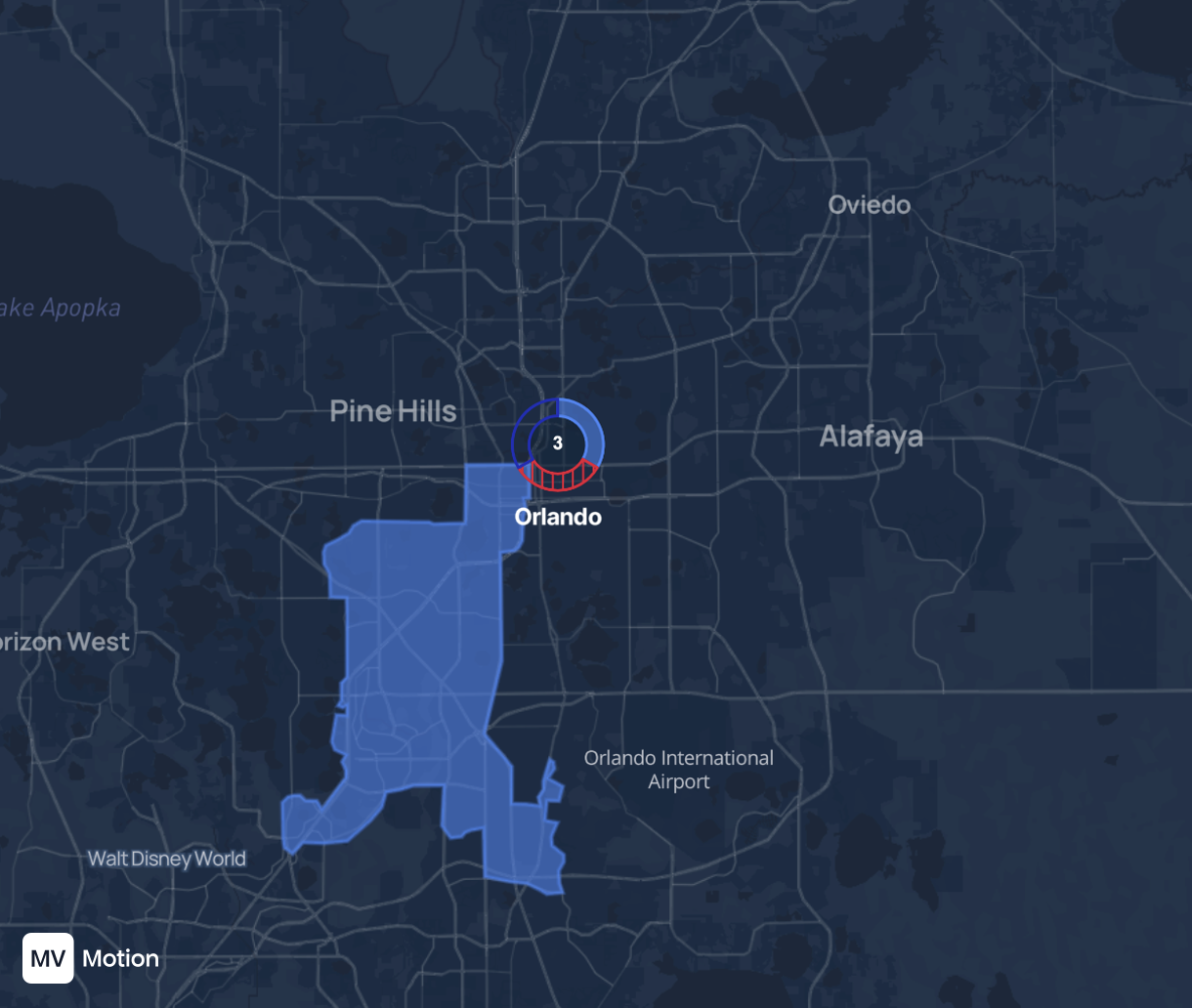

Waymo is adding Portland to its expansion pipeline, beginning with manually driven mapping and data collection across the city’s bridges, wet corridors and urban streets, but with no paid robotaxi launch date yet as Oregon's laws do not yet permit autonomous operations. Mobileye/MOIA is also moving from concept toward deployment: more than 100 autonomous VW ID. Buzz vehicles are now being tested across six cities, with Orlando, Florida selected for MOIA’s initial U.S. launch, with onboard human supervisors first.

Waymo pledged first Oregon launch

Source: RobotaxiMap.com

Mobileye testing in Orlando

Source: RobotaxiMap.com

Disclaimer

This report and the information within are not investment advice or an offer to sell or a solicitation of an offer to buy any security or other financial instrument. Neither the Firm nor any person related to the Firm (“We” or “Our”) are offering, selling or buying any security to or from any person through this research report. We do not provide investment advice. You understand and agree that We do not have an investment advisory relationship with you and do not owe you any fiduciary duty. You agree that use of the research presented in this report is at your own risk and that you will do your own research and due diligence beforemaking any investment decision regarding any securities related to any issuer(s) discussed herein (“Covered Issuer”) or any other financial instruments that reference the Covered Issuer or any securities issued by the Covered Issuer. You represent that you have sufficient investment sophistication to critically assess the information, analysis and information presented in this report. You further agree that you will not communicate the contents or information in this report to any other person. This report reflects and expresses Our analysis as of the time of the report only. This report is based on generally available information, field research, inferences and deductions through Our due diligence and analytical process. To the best of Our ability and belief, all information contained herein is accurate and reliable, is not material non-public information, and has been obtained from public sources that We believe to be accurate and reliable. Further to the best of Our ability and belief, all information has been obtained from sources that are not insiders or connected persons of any Covered Issuers or who may otherwise owe a fiduciary duty, duty of confidentiality or any other duty to the Covered Issuer (directly or indirectly). However, such information is presented “as is,” without warranty of any kind, whether express or implied. With respect to the report, We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or regarding the results to be obtained fromits use. Further, this report only contains Our analysis and information. All information in the report is subject to change without notice, and We will not update or supplement this report or any of the information, analysis or information contained therein. We generally invest in broad based and sector related indexes, typically via mutual funds and exchange traded funds. As of the publication date of this report, We also have positions in Tesla, Nvidia, and other individual companies. Thus, We will realize gains if the prices of these securities appreciate. We may trade in Tesla and/or Nvidia stock, the other securities, or the indexes after this report, and such position(s) may be long, short, or neutral at any time hereafter regardless of the comments, information, or views stated in the report. We will not update this report or information to reflect changes in any positions held or any trades.