/

Send us an emailinfo@mvmotion.com

© 2026 MV Motion All rights reserved.

All Research / Robotaxis & Autonomy, Humanoid Robots

In our inaugural monthly newsletter, we comment on the top recent stories and highlight new deployments on the RobotaxiMap.com.

The newsflow in robotaxis and humanoid robots can be overwhelming. Each month, Martin Viecha and the MV Motion team will summarize the most important news stories, share our perspective, and comment on the latest deployments on RobotaxiMap.com. Stay on top of the industry in 5 minutes - or dig deeper, if you prefer!

This month, we present you with 6 stories and 4 Robotaxi Map updates.

Uber announced Uber Autonomous Solutions, a new product suite to help Uber's Robotaxi partners to commercialize faster and at a lower cost per mile. It packages Uber’s capabilities across infrastructure, user experience, and fleet operations - including AV 2.0 training data (built with engineers from the newly launched Uber AV Labs), data-enriched mapping, regulatory support, and fleet financing; plus in-car UX, complex product use cases, and end-to-end customer support; and fleet tools like AV Mission Control, remote assistance, field ops, and AV-specific insurance. This follows a $100M investment into robotaxi charging infrastructure announced earlier.

Uber wants to become the booking.com in the world of multiple robotaxi companies: While the robotaxi companies can focus on perfecting software, Uber wants to provide the "boring" but essential parts of robotaxi deployment, such as dispatch and pricing, teleoperation, scale of its network, charging, and servicing. This move allows smaller robotaxi firms to optimize utilization of their fleets from day one, while Uber retains ownership of the customer experience. It's really a strategy of "if we can't compete with Waymo, we'll bundle together all other robotaxi players". While there are many companies outside of China who want to run robotaxi fleets, few have been able to deliver. We covered this topic in our report The forgotten Robotaxi Race: Race to build Infrastructure.

Wayve, an autonomous driving startup from the UK, announced its $1.5B funding round at $8.6B valuation as a major step toward commercialization, highlighting the addition of Mercedes and Stellantis as new strategic OEM partners. These automakers expand Wayve’s growing industry footprint alongside Nissan, which has also contributed to the investment on top of its last year’s commitment to bring Wayve’s self-driving tech into its cars. The financing also underscores continued backing from influential technology and platform players such as Uber, NVIDIA, or Microsoft, and premier investors like Balderton or SoftBank. Wayve is expecting to start robotaxi trials in 2026 and deploy advanced driver assistance into consumer cars starting in 2027.

Wayve, Europe's leading autonomy startup, pioneered end-to-end AI-based autonomy. That's right, Wayve was working end-to-end AI autonomy before Tesla did. As we described in our report Which Carmakers are mass-collecting Data for AI autonomy?, there are now ~10 carmakers working on end-to-end AI based autonomy. What does Tesla or BYD have that Wayve doesn't? Mass collection of real-world driving data. This is where Wayve could use some help, which is why commitments from large carmakers is important here. That said, how quickly these carmakers will be able to move to implement Wayve's tech is yet to be seen.

Hyundai is advancing its robotics push on two fronts: it has hired former Tesla Optimus leader Milan Kovac as an adviser and plans to nominate him to Boston Dynamics’ board. Reuters also reports that Boston Dynamics CEO Robert Playter is stepping down after more than 6 years, a move investors interpreted as a sign that Hyundai wants faster execution beyond R&D. The company recently unveiled the production Atlas robot and plans to deploy humanoids at its automotive plant in Georgia, with capacity targeted at 30,000 units annually by 2028.

Hyundai share price has tripled in the past 6 months, and it's not because company's profitability. While Figure AI reached a valuation of ~$40B less than a year ago, it is now becoming clear that Boston Dynamics is becoming Hyundai's highest value assets. Recent video of Atlas's human-like movements clearly made an impact. Additionally, Milan Kovac, who along with his team built one of the most competitive humanoid programs globally (going from a dancer in a robot suit to an actual dancing robot in under 4 years), is joining Boston Dynamics board. Lastly, Hyundai will be deploying its robots at its car factory. So now, we have the Agility Robotics Digit deploying at Toyota factory, as well as numerous advanced pilots - Tesla Optimus at the Tesla factory, Figure AI robot at the BMW factory, and Boston Dynamics E-atlas building cars for Hyundai. While it will take time for humanoids to do real, generalizable work with no oversight, the race is very much on.

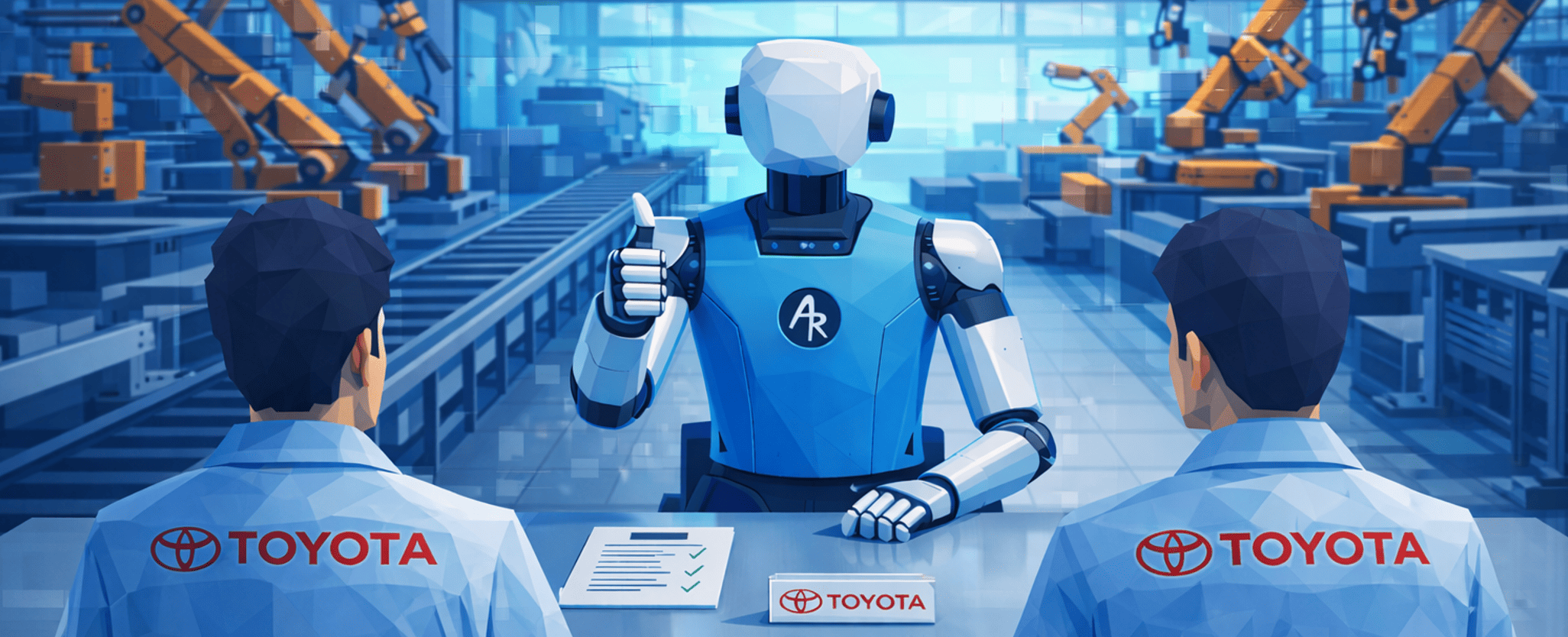

Agility Robotics said it has signed a commercial Robots-as-a-Service agreement with Toyota Motor Manufacturing Canada (TMMC) to deploy its humanoid robot Digit in real production following a successful year-long pilot. Under the deal, multiple Digit units will support manufacturing, supply chain, and logistics tasks at TMMC’s Woodstock, Ontario assembly plant, aiming to improve efficiency and reduce physically demanding work for employees. The agreement marks a shift from pilot trials to operational use of humanoid robots in automotive production.

Agility’s Toyota deal stands out because it is not just another pilot: it follows a successful trial and moves into a commercial RaaS deployment of the humanoid robot called Digit, inside a real auto plant workflow (parts handling/logistics), with Toyota having evaluated a number of robots before choosing Digit. This marks one of the first real world examples of where humanoid robots actually take on the task of humans - not just pose for a well-lit, beautifully-shot promotional videos.

New York Governor withdrew a proposal that would have legalized commercial robotaxi services in smaller cities outside of NYC, dealing a setback to Waymo’s expansion plans this year. The measure, pulled after insufficient legislative support, would have let autonomous-vehicle firms operate without onboard safety drivers outside NYC. Waymo says it remains committed to working with lawmakers, but the reversal stalls access to a major ride-hailing market.

The data is clear: Unsupervised Waymo robotaxis reduce injury-causing collisions by 82% and they reduce pedestrian injury-causing collisions by a staggering 92%. In spite of this, legislative support is lagging behind. While California's DMV already gave a permit to Waymo for 70% of California's population (read our report on the topic), NY is pushing back. The bottom line is that while many US states and China have welcomed Robotaxis, some US states and many European countries are pushing back. Just like Uber's journey in early days wasn't easy due to slow legislation, this will likely be the case with robotaxi deployment for years to come.

Waabi secured $1B in new funding to power a planned 25,000-vehicle robotaxi deployment with Uber, marking a strategic shift from trucking toward personal autonomy. The raise includes an oversubscribed $750 million Series C led by Khosla Ventures and G2 Venture Partners, with additional capital from Uber.

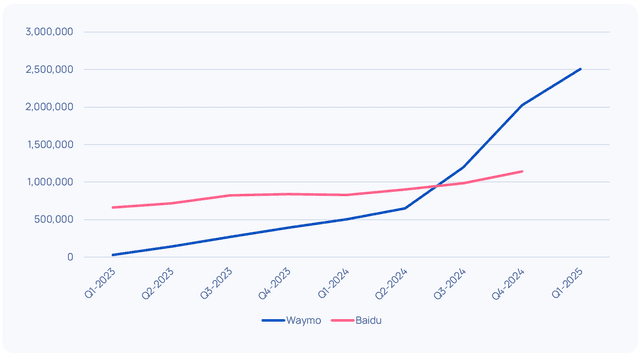

From simulation to the real world: Waabi is a relatively less known startup compared to the likes of Waymo, Zoox or Tesla. The company is betting on perfecting the simulation to the extent that their software will understand every nuance of a physical world. We shouldn't forget that Waymo too has its Waymo World Model announced less than a month ago in addition to its 200 million unsupervised robotaxi miles. If a world model itself manages to reach robotaxi-level autonomy far safer than a human is yet to be seen. But if it does, it could open doors to other companies that are building similar world models, to ultimately join the robotaxi race.

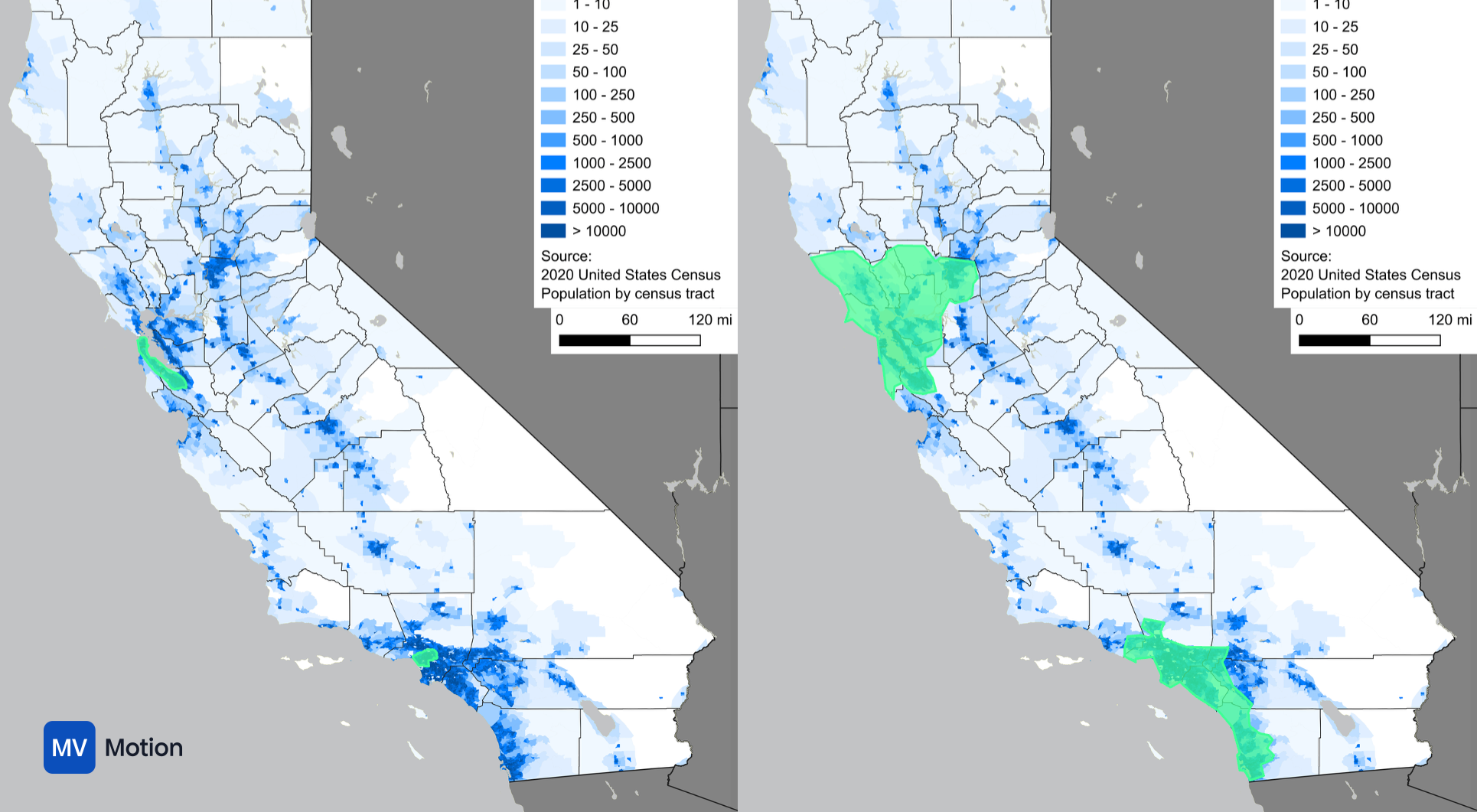

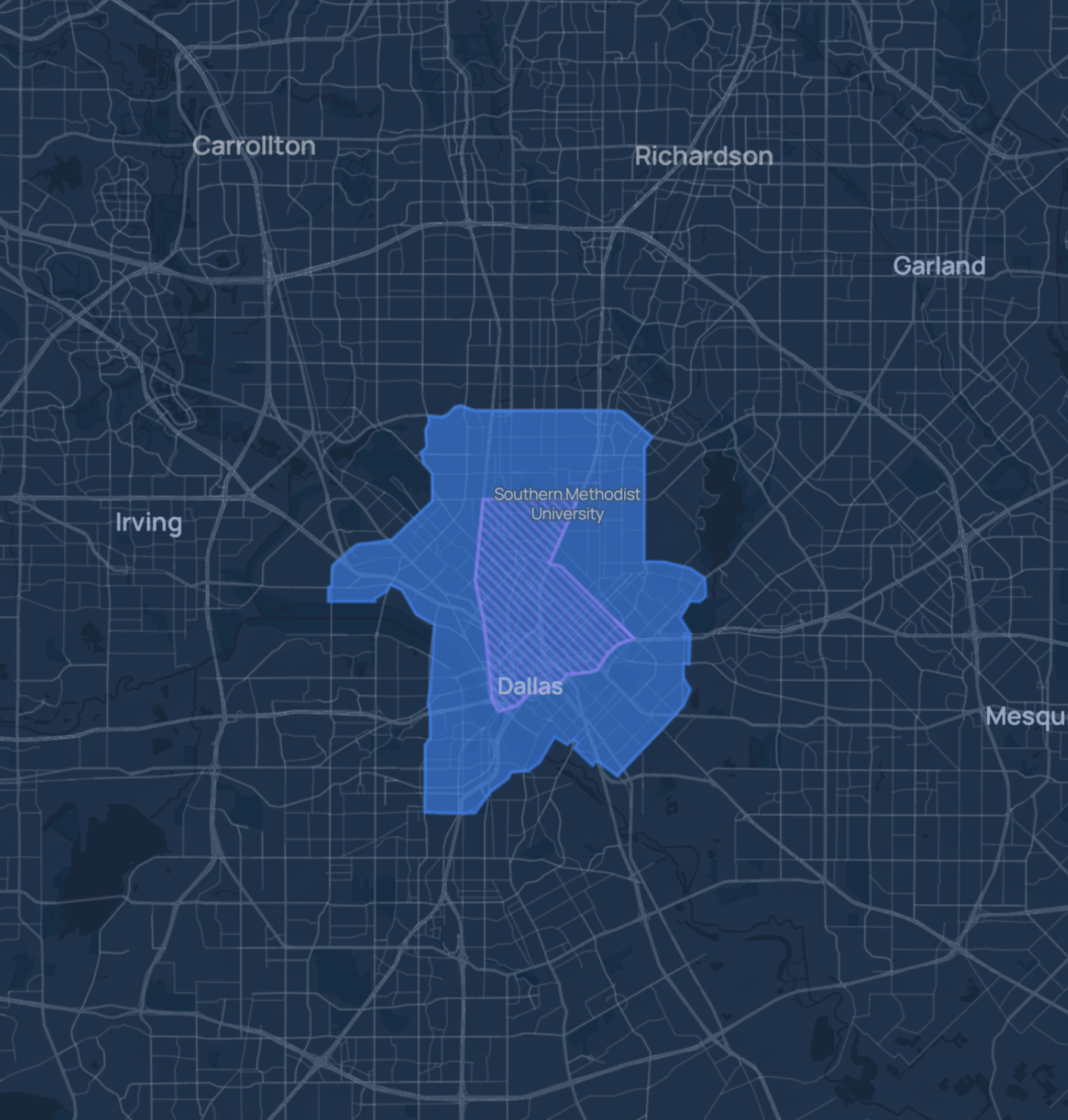

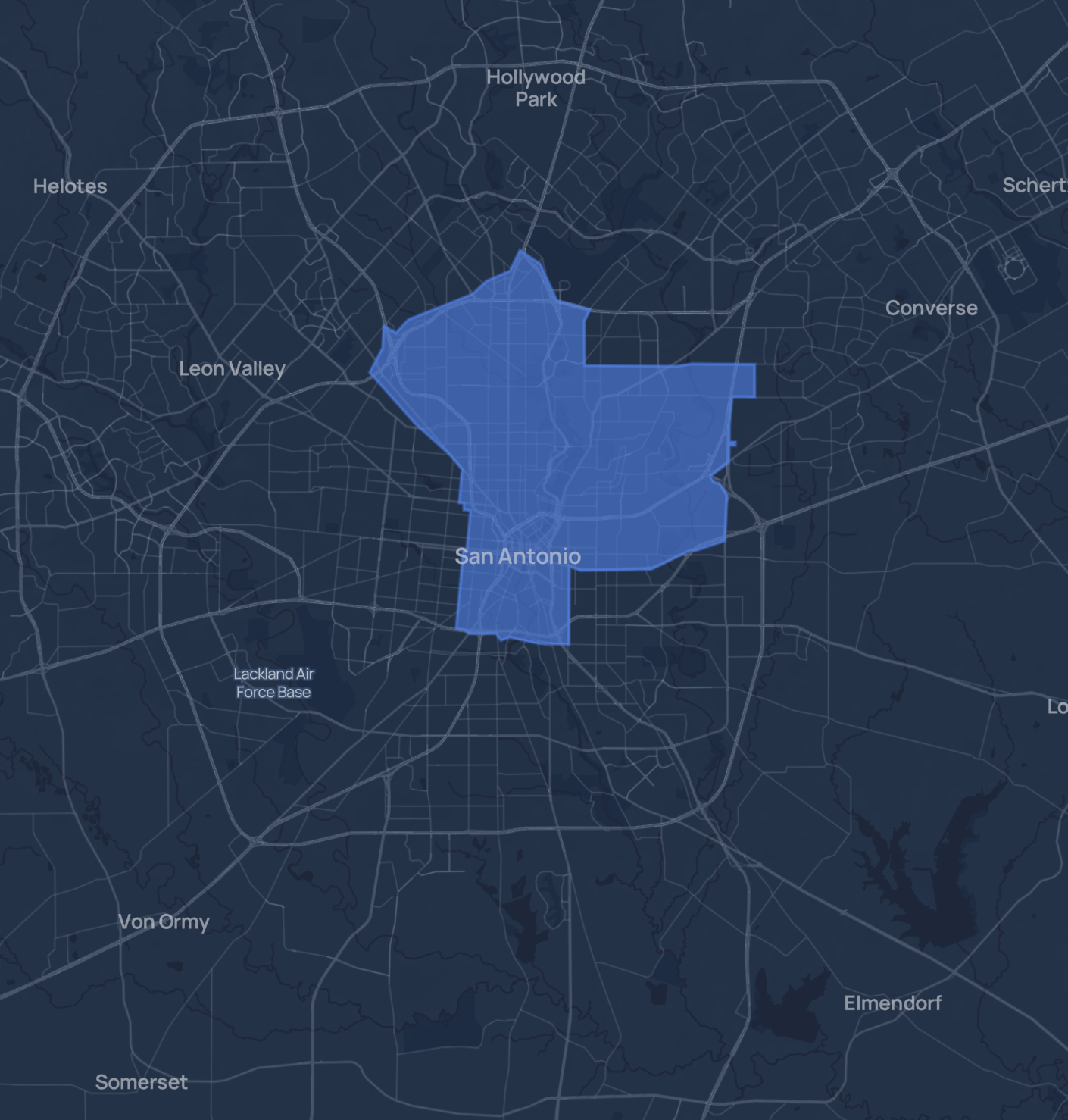

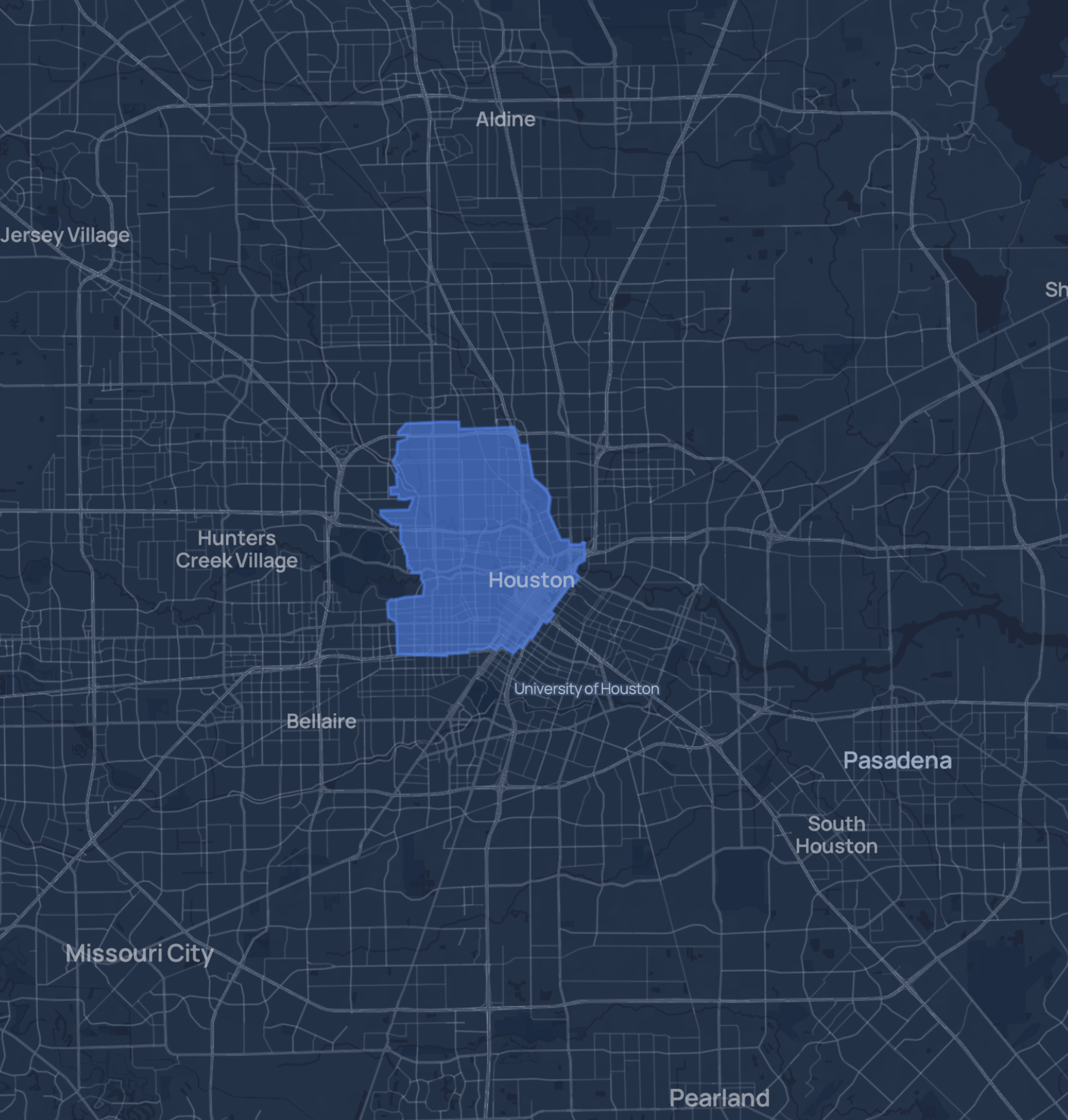

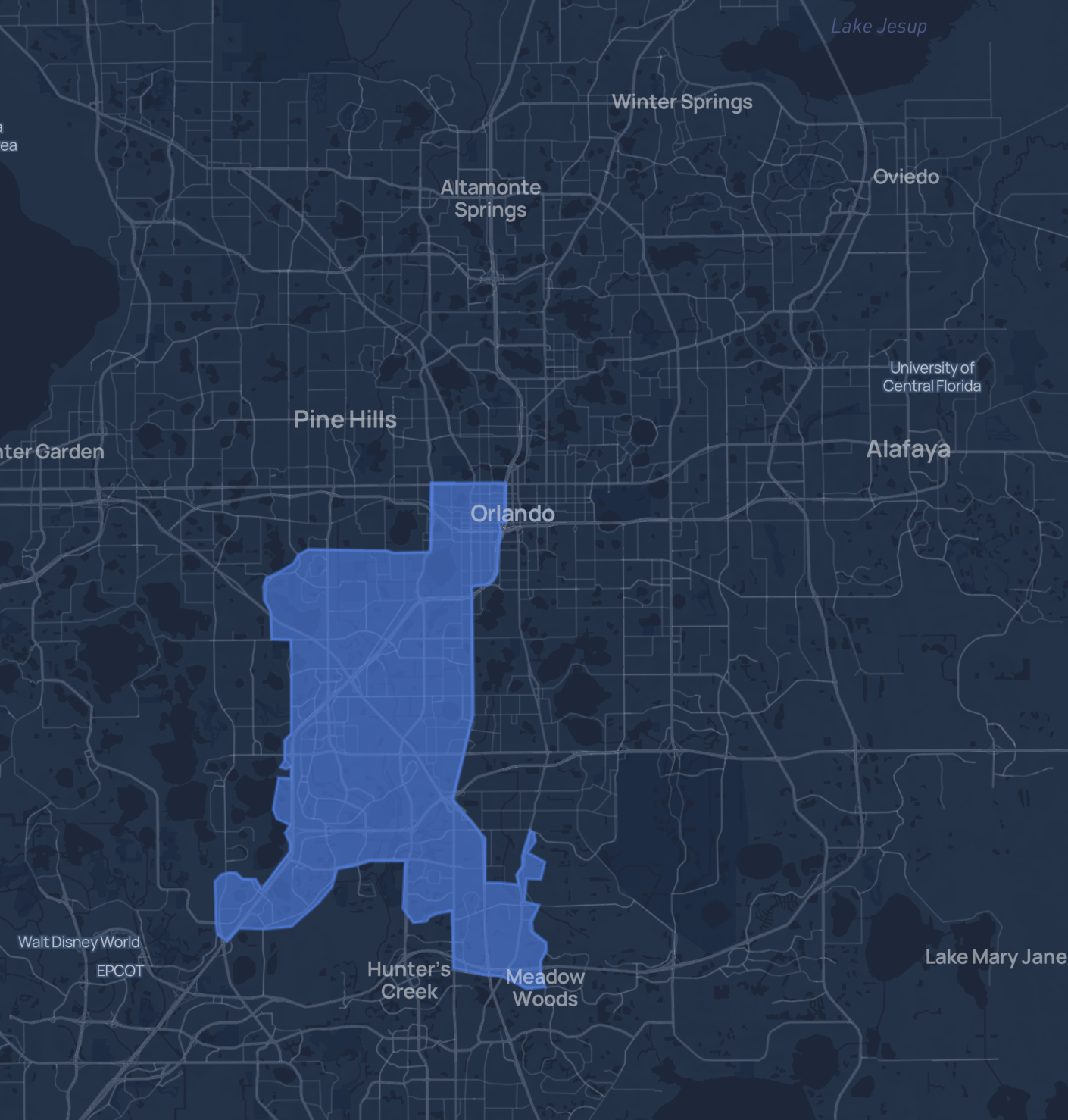

Waymo has just launched a fully driverless robotaxi service in 4 new U.S. cities - Dallas, Houston, San Antonio, and Orlando - bringing full driverless operations to 10 US metropolitan areas. This rollout adds direct coverage of around 0.9 million residents, giving Waymo first-mover advantage over Tesla, which also announced intention to launch in some of the newly started locations. Notably, Waymo has not partnered with Uber in any of the deployments. In Dallas, Waymo even clashes with Uber and its partner Avride (formerly Yandex), which currently run supervised rides across the city's downtown.

Dallas

San Antonio

Houston

Orlando

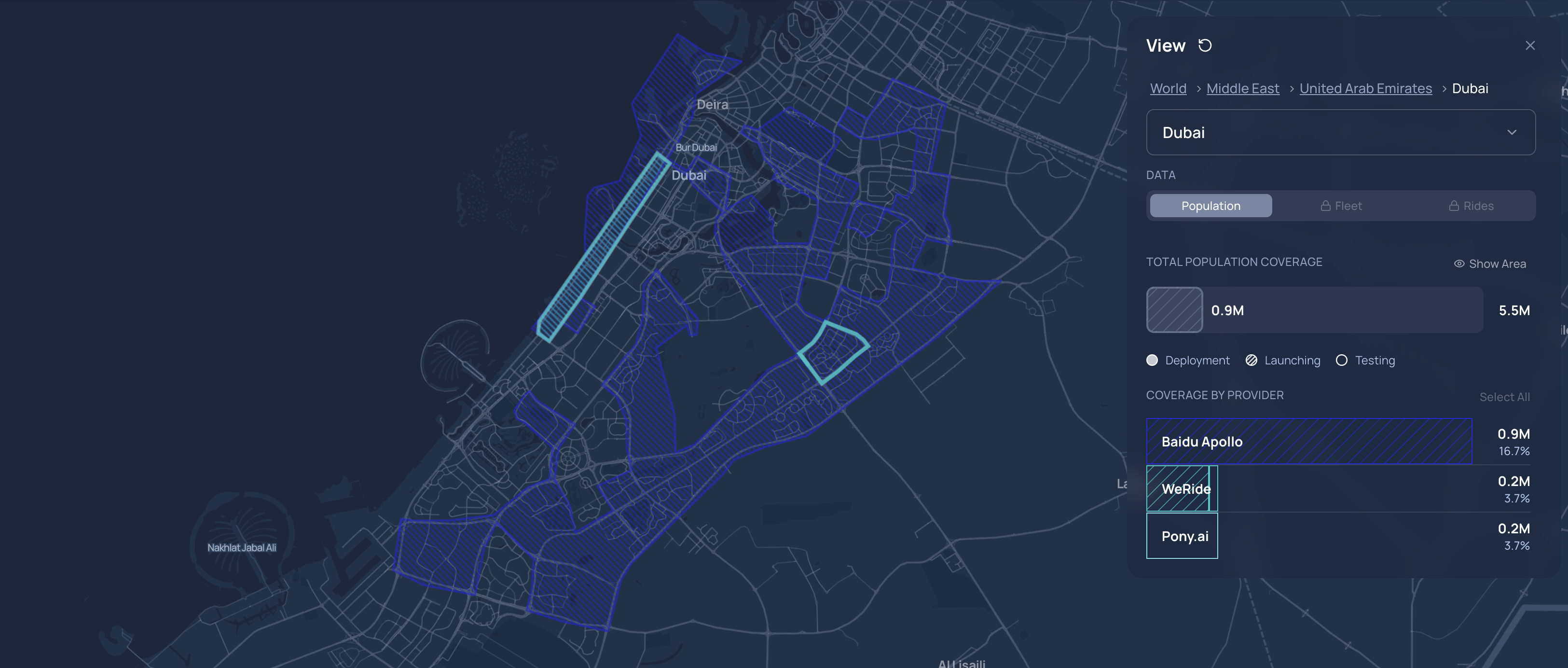

Dubai is gearing up for an exciting era of autonomous mobility, with several robotaxi launches planned. Baidu’s Apollo Go is poised to begin fully driverless service soon (most likely in March), expanding across two RTA-designated AV Zones that cover key parts of the city and laying the groundwork for a fleet of over 1,000 vehicles in years ahead. Meanwhile, WeRide’s trial has already begun in Jumeirah and Umm Suqeim via the Uber app, currently with safety specialists onboard as part of the broader rollout to fully driverless rides. Pony.ai is also testing robotaxis in Dubai as it prepares for expanded autonomous operations.

The robotaxi race in Abu Dhabi is clearly picking up steam, with WeRide and Uber leading the charge: their service now covers roughly 70 % of the city’s core, having expanded from Al Reem, Al Maryah, Yas and Saadiyat to include Corniche Road, Sheikh Zayed Grand Mosque, Khalifa City, Masdar City and Rabdan downtown, leveraging its full city coverage permit. Baidu has also rolled out its robotaxi service in January, starting with fully driverless rides on Yas Island (with AutoGo) and planning broader coverage across the emirate. Pony.ai is set to follow with driverless launch scheduled for 2026, with Momenta and Didi also laying early groundwork for deployment.

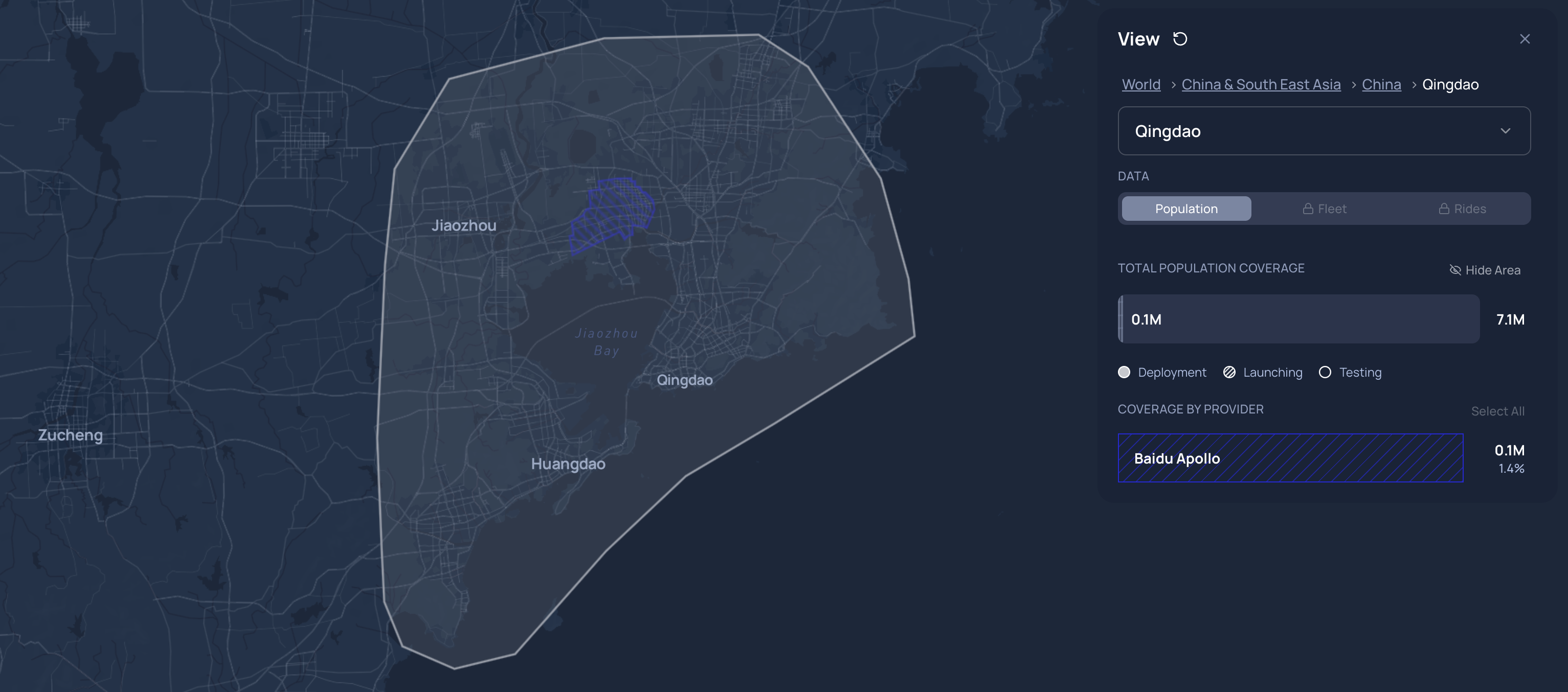

In Qingdao, Baidu’s Apollo Go robotaxi service has begun a trial operation, initially reaching a catchment area of about 100k people within the defined zone visible in the app. Although Qingdao does not enjoy the same international recognition as, say, San Francisco Bay Area - the 2 agglomerations are fairly similar in population size (around 7m people). This highlights Qingdao’s future potential as one of many Chinese megacity robotaxi hubs.

Disclaimer

This report and the information within are not investment advice or an offer to sell or a solicitation of an offer to buy any security or other financial instrument. Neither the Firm nor any person related to the Firm (“We” or “Our”) are offering, selling or buying any security to or from any person through this research report. We do not provide investment advice. You understand and agree that We do not have an investment advisory relationship with you and do not owe you any fiduciary duty. You agree that use of the research presented in this report is at your own risk and that you will do your own research and due diligence beforemaking any investment decision regarding any securities related to any issuer(s) discussed herein (“Covered Issuer”) or any other financial instruments that reference the Covered Issuer or any securities issued by the Covered Issuer. You represent that you have sufficient investment sophistication to critically assess the information, analysis and information presented in this report. You further agree that you will not communicate the contents or information in this report to any other person. This report reflects and expresses Our analysis as of the time of the report only. This report is based on generally available information, field research, inferences and deductions through Our due diligence and analytical process. To the best of Our ability and belief, all information contained herein is accurate and reliable, is not material non-public information, and has been obtained from public sources that We believe to be accurate and reliable. Further to the best of Our ability and belief, all information has been obtained from sources that are not insiders or connected persons of any Covered Issuers or who may otherwise owe a fiduciary duty, duty of confidentiality or any other duty to the Covered Issuer (directly or indirectly). However, such information is presented “as is,” without warranty of any kind, whether express or implied. With respect to the report, We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or regarding the results to be obtained fromits use. Further, this report only contains Our analysis and information. All information in the report is subject to change without notice, and We will not update or supplement this report or any of the information, analysis or information contained therein. We generally invest in broad based and sector related indexes, typically via mutual funds and exchange traded funds. As of the publication date of this report, We also have positions in Tesla, Nvidia, and other individual companies. Thus, We will realize gains if the prices of these securities appreciate. We may trade in Tesla and/or Nvidia stock, the other securities, or the indexes after this report, and such position(s) may be long, short, or neutral at any time hereafter regardless of the comments, information, or views stated in the report. We will not update this report or information to reflect changes in any positions held or any trades.