/

Send us an emailinfo@mvmotion.com

© 2026 MV Motion All rights reserved.

All Research / Automotive & EVs, Robotaxis & Autonomy, +1 more

The July newsletter highlights key developments across Waymo’s entry into Europe, upcoming IPOs, humanoid robot updates and more. RobotaxiMap.com also recorded several notable updates, including planned robotaxi launches in Zurich and Madrid, new entrants coming to Houston and Miami, and geofence expansions.

The newsflow in robotaxis and humanoid robots can be overwhelming. Each month, Martin Viecha and the MV Motion team summarize the most important news stories, share our perspective, and comment on the latest deployments on RobotaxiMap.com. Stay on top of the industry in 5 minutes - or dig deeper, if you prefer!

This month, we present you with 8 exciting news story picks and 5 Robotaxi Map deployment updates!

Waymo is quietly laying the groundwork for a broader European expansion, registering local entities across several European countries. This marks the first signal of Waymo entering the EU, bracing for taking on Chinese robotaxi companies that have been actively pursuing EU roll-out for several months now.

Europe is likely to become the ultimate battleground between Chinese, American and European robotaxi companies. Such competition is not allowed in the US or China. When it comes to business models, Waymo has built its lead through a relatively vertically-integrated operating model, but Chinese rivals are increasingly expanding through local partners: WeRide, for example, is using Uber for distribution while working with third-party fleet operators to pursue a more asset-light rollout.

Waymo and Uber ended their robotaxi partnership in Phoenix, with Waymo vehicles no longer available through Uber’s app after nearly three years. Uber said the pilot ended at its contracted end date and is preparing a new AV partnership in the market, while Waymo returned the vehicles to its own fleet. The partnership involved just over a dozen Waymo vehicles and completed hundreds of thousands of Uber trips, while Waymo remains available through Uber in Austin and Atlanta.

While we still believe that ridehailing companies will act as "booking.com" for smaller robotaxis companies, it is becoming clearer that Waymo is increasingly doing it alone. Waymo launched five new cities in recent months, all of which solely with their in-house ridesharing app, and no ridehailing partners. This feels like the next step in the same direction.

Zoox unveiled an updated version of its purpose-built robotaxi, refining the vehicle’s design ahead of broader commercial service. The core platform remains unchanged, including the steering-wheel-free cabin, bidirectional driving, carriage-style seating, moonroof, and 40-sensor perception suite.

We applaud Zoox's vehicle design as truly autonomy-first design. The challenge is that the capacity for this vehicle is just 100/week or 5k/year, which we think is not competitive enough. Other robotaxi makers are likely to launch far more than 10k robotaxis in 2027. For a true land-grab strategy, the capacity needs to be higher.

Waymo faced resident complaints in June over robotaxis crowding the shared garage at San Francisco’s Soma Grand condo complex. Residents said Waymo vehicles queued at entrances and exits, got stuck in tight garage spaces, and added several minutes to daily commutes, with some delays estimated at 15–20 minutes. Waymo said it added resident charging stations, free visitor parking, parking-cost coverage, safety mirrors, and speed bumps as means to get into the residents' good grace - but past instances show that this is no easy feat.

We have long argued that infrastructure buildout is going the be the main bottleneck for robotaxi deployment for any company that truly solves robotaxi software (there are not many of those). Figuring out how to park, charge, clean and maintain thousands of robotaxis in each city, will certainly have impact on neighborhoods, particularly due to the intent to maximize robotaxi utilization rate. Building robotaxi parking capacity will come with challenges that are not yet commonly understood.

Momenta Global launched its Hong Kong IPO, seeking to raise up to $750 million to fund autonomous-driving R&D and robotaxi rollout, with trading expected to begin on July 8. Momenta plans to use about 60% of the proceeds to increase R&D spending, increasing AI computing power, data storage and engineering staff, while about 20% will support faster rollout of its Robotaxi services. Momenta's software was used in 680k vehicles including brands such as Mercedes, Toyota, BYD and others.

After Pony.AI and WeRide, we see yet another Chinese autonomous driving company IPO. Momenta is pushing for wider ADAS rollout, as well as robotaxi launch in Munich and Abu Dhabi. Nevertheless, sustained financing remains critical: Pony.ai and WeRide still trade down YTD, despite rapid growth, early signs of profitability, and breakeven economics in some cities. Building a competitive robotaxi market will require patient capital willing to back several credible contenders through the long road to scale.

NVIDIA announced Halos for Robotics, a full-stack safety system for robotics and physical AI. The system combines IGX Thor compute, Holoscan Sensor Bridge, Halos OS, and NVIDIA’s AI Systems Inspection Lab to support safety functions, sensor connectivity, validation, and certification preparation. Agility is the first robotics company using Halos for its Digit humanoid in industrial settings.

It's increasingly feeling like humanoid software and humanoid hardware will often be made by different companies. In addition, it seems like Nvidia would like to provide not only the AI compute for humanoids (and robotaxis), but also the software itself. The "safety system" software could be the first of many steps towards an end-to-end humanoid software stack.

Agility Robotics agreed to go public through a merger with Churchill Capital Corp XI at a $2.5B pre-money equity value. The transaction is expected to provide more than $620M in gross proceeds, with $420M in cash and $200M of incremental financing via PIPE, with the combined company expected to trade as AGLT. Agility's humanoid, Digit, is already operating with customers including Schaeffler, GXO, Toyota Motor Manufacturing Canada, and Mercado Libre, with 65,000+ operating hours and $300M+ of multi-year Digit v5 orders secured (subject to milestones).

As we highlighted in our humanoid robotics report Can Humanoid Robots do any actual Work?, Agility is one of the few companies that has moved beyond demos and into commercial deployment. Its operating hours, customer roster, and order backlog give it a stronger foundation than most peers. The next challenge is broader task generalization: to justify its valuation and long-term potential, Digit (Agility's humanoid robot) will need to progress beyond repetitive tote-moving workflows and prove it can perform a wider range of economically valuable tasks across industrial environments.

BMW is deploying Figure 03 humanoid robots at its Spartanburg plant to expand the use of physical AI in production. Figure 03 succeeds Figure 02, which supported production of more than 30,000 BMW X3 vehicles, and will perform logistics sequencing tasks using upgraded hands, tactile sensors, and safety features. The deployment is part of BMW's broader effort to integrate humanoid robots into manufacturing.

Figure AI's latest generation humanoid robot already performed impressively sorting out packages, it will be interesting to see how it performs at BMW's production plant. Ultimately, we need to see announcements that humanoid robots have taken over a specific job at a factory on a 24/7 basis, not just a pilot or a trial. Perhaps, Figure 03 will be the humanoid that gets us there.

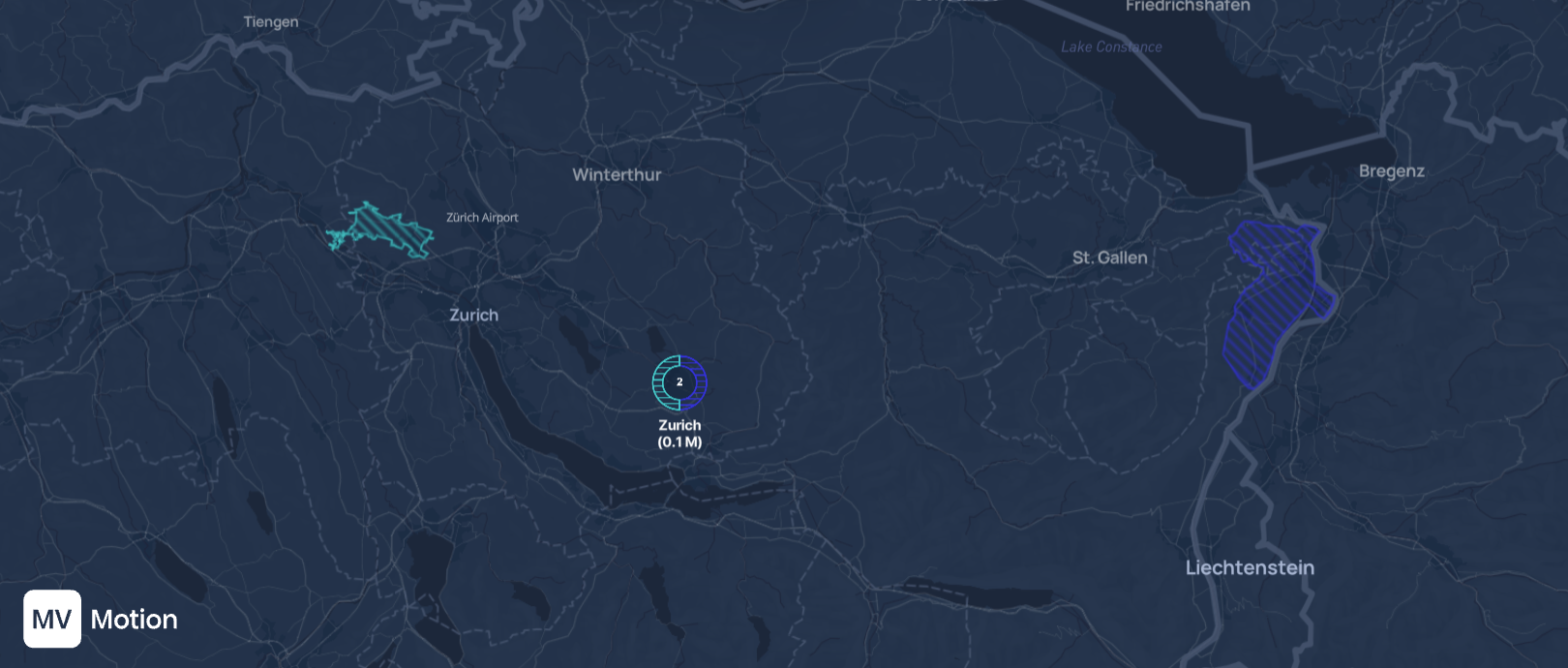

WeRide and Uber plan to launch commercial robotaxis in the Greater Zurich Region later this year via the Uber app, with Rydera operating the fleet and a gradual path toward fully driverless service. Baidu’s Apollo Go is also entering Greater Zurich/Eastern Switzerland through PostBus’s AmiGo service, creating a rare early European head-to-head between Chinese AV companies. This market stands out because Switzerland is European but non-EU (so not directly subject to wider EU regulation harmonization efforts), and because Alpine winter conditions make this one of the first real robotaxi deployments where snow is unavoidable. As we have pointed out in the reports All About the Weather, and Can Ride-hailing Survive the Age of Autonomy, bad weather remains one of the key technological bottlenecks to growth. We are very curious to see how this will be dealt with in a real commercial setting.

WeRide and Baidu in Northeastern Switzerland

Source: RobotaxiMap.com

WeRide, Uber and AVOMO are bringing a robotaxi pilot to Madrid, marking WeRide and Uber’s first joint market entry in the EU, and Spain’s first planned robotaxi pilot. The service is expected to launch later this year through the Uber app, initially as supervised rides, before scaling toward unsupervised robotaxi operations across core urban areas. The Madrid rollout is part of WeRide and Uber’s broader 15-city partnership, with AVOMO (Waymo's teleoperations partner in Atlanta and Phoenix, where Waymo has been deploying with Uber) supporting fleet operations and the partners targeting hundreds of robotaxis in Madrid as performance milestones are met.

WeRide's second EU announced launch, after Bratislava

Source: RobotaxiMap.com

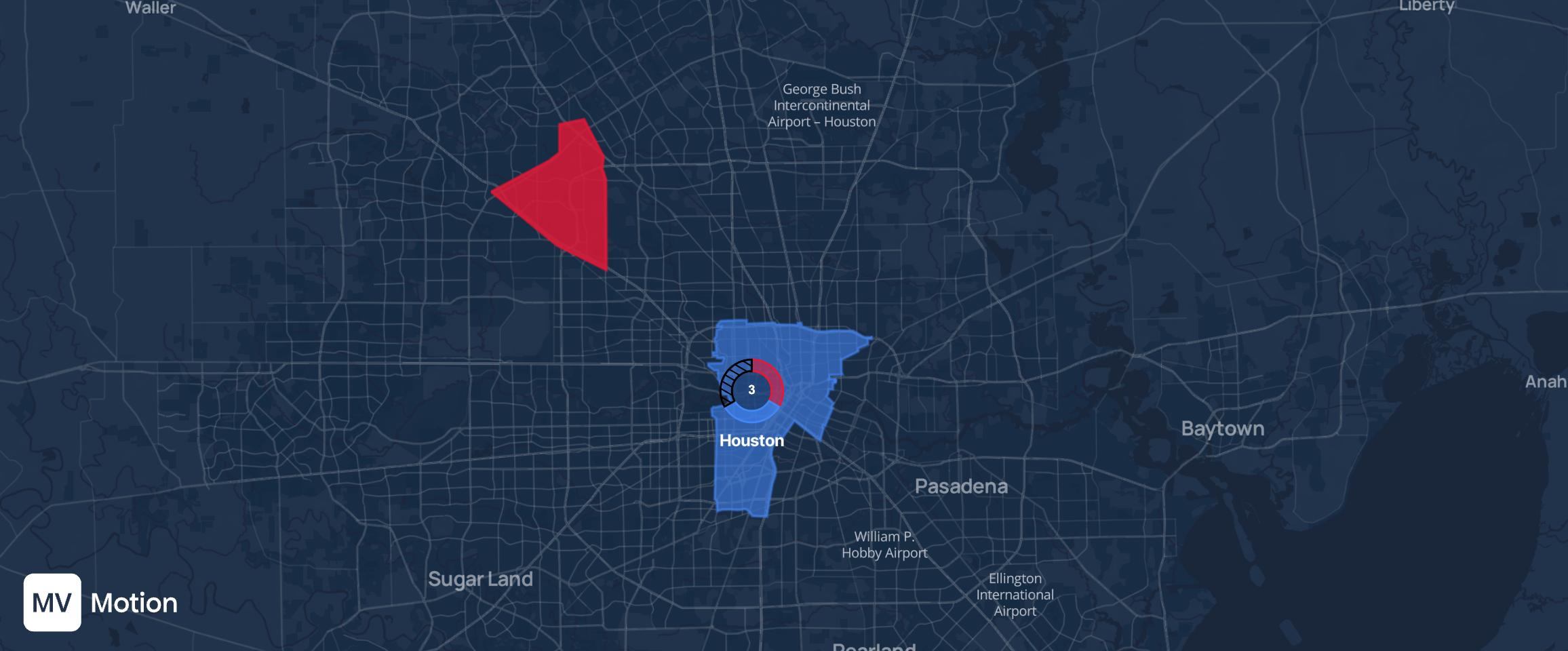

Houston is on course to become a three-way robotaxi battleground, with Uber, Nuro and Lucid planning to launch a robotaxi service in the city by mid-2027. The launch would put Uber into direct competition with Waymo and Tesla, bringing the largest ride-hailing network, the leading scaled robotaxi operator and Tesla’s vertically integrated autonomy push into the same market. Nuro is already running 24/7 supervised testing, while Uber has secured a 50,000-square-foot Houston depot and an additional pitstop to support future robotaxi fleet operations.

Nuro robotaxis will follow established Waymo and Tesla operations

Source: RobotaxiMap.com

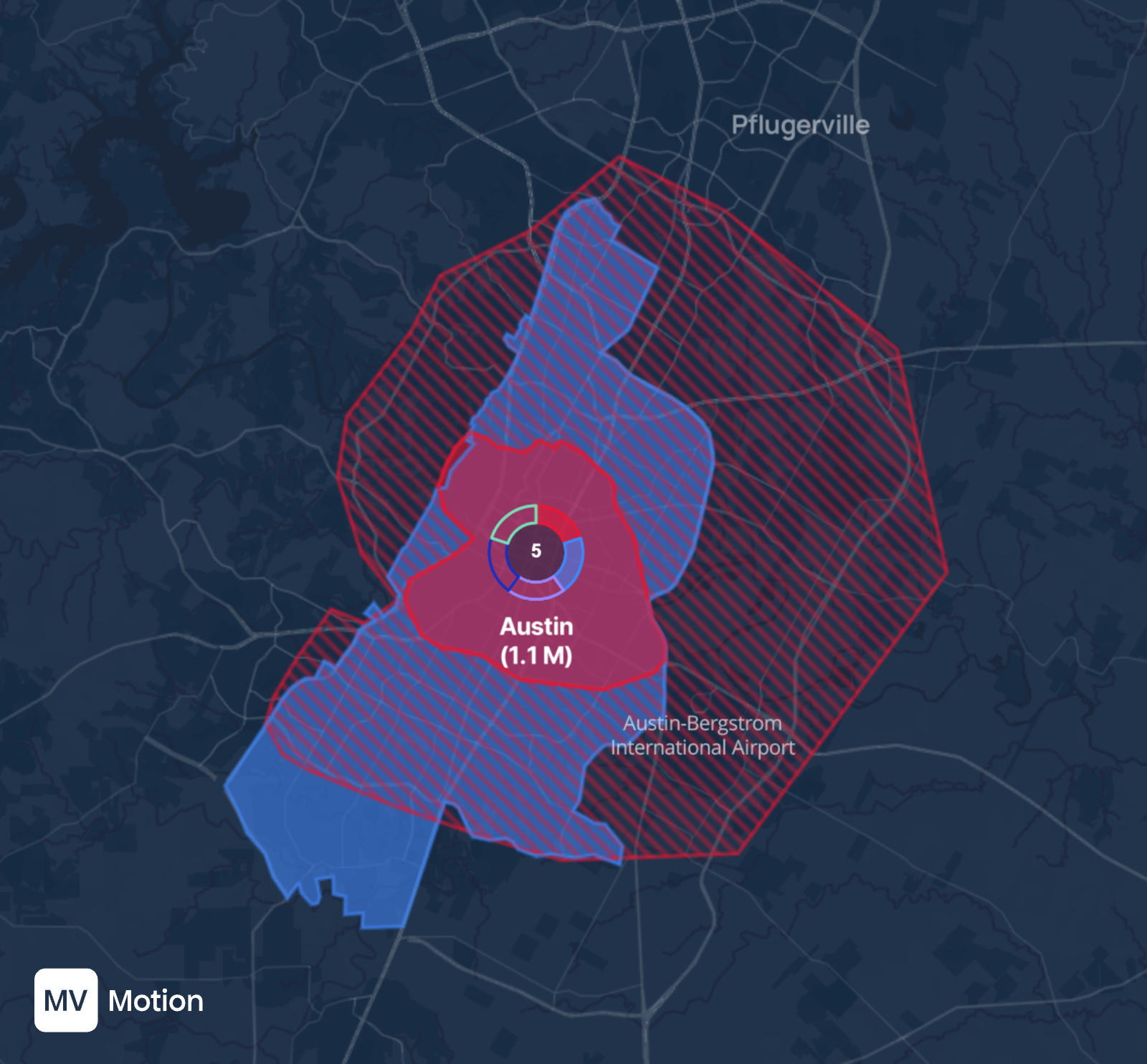

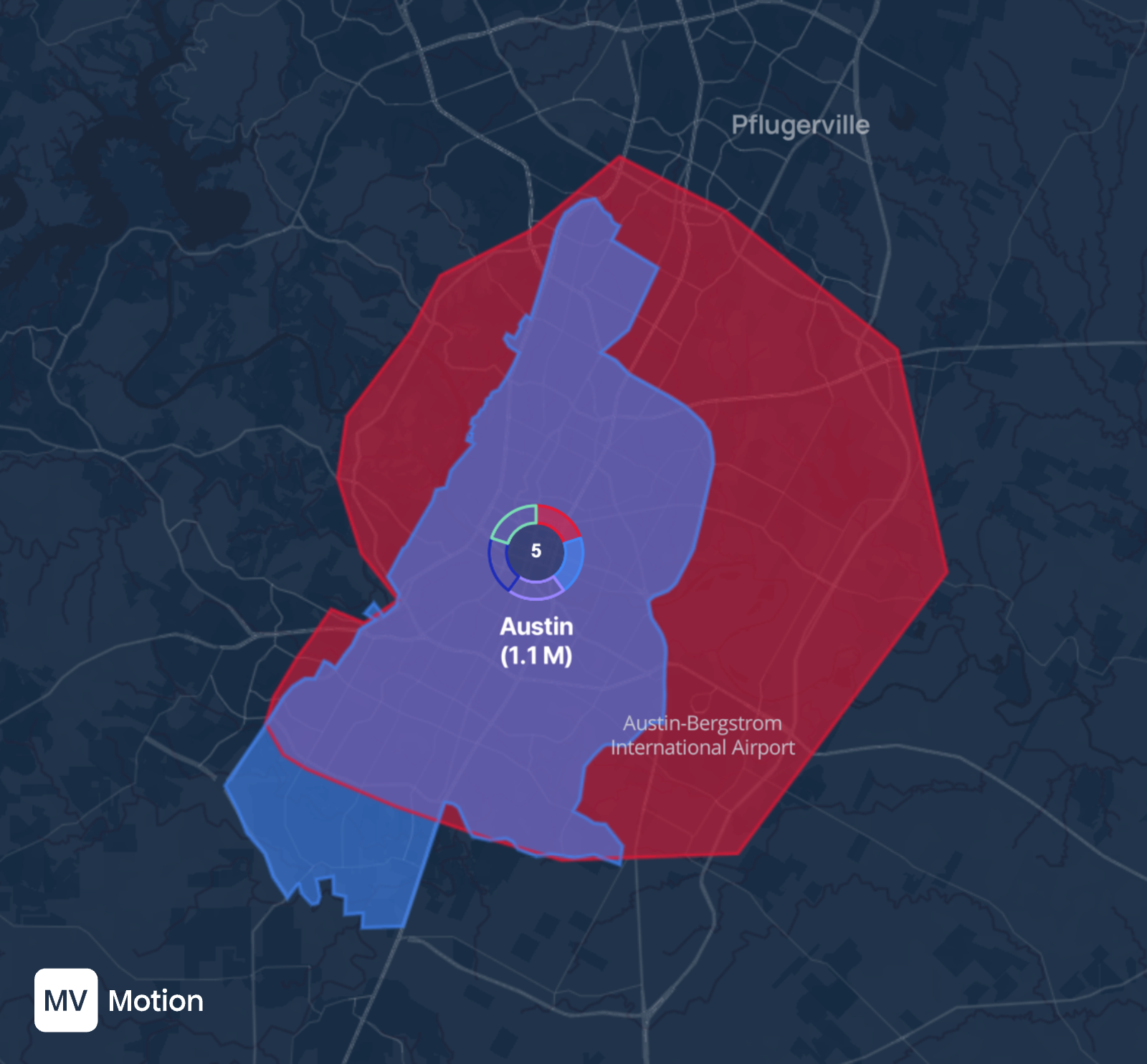

Tesla expanded its Austin unsupervised robotaxi program in June, rolling out robotaxis across the Austin Metro area after nearly a year of operating the service in the city. Tesla has also begun supervised public-road testing of its first production Cybercab in Austin, with a safety monitor in the passenger seat, while the unsupervised paid robotaxi service still uses Model Y vehicles rather than the purpose-built Cybercab.

Old Tesla unsupervised ODD

Source: RobotaxiMap.com

New Tesla unsupervised ODD

Source: RobotaxiMap.com

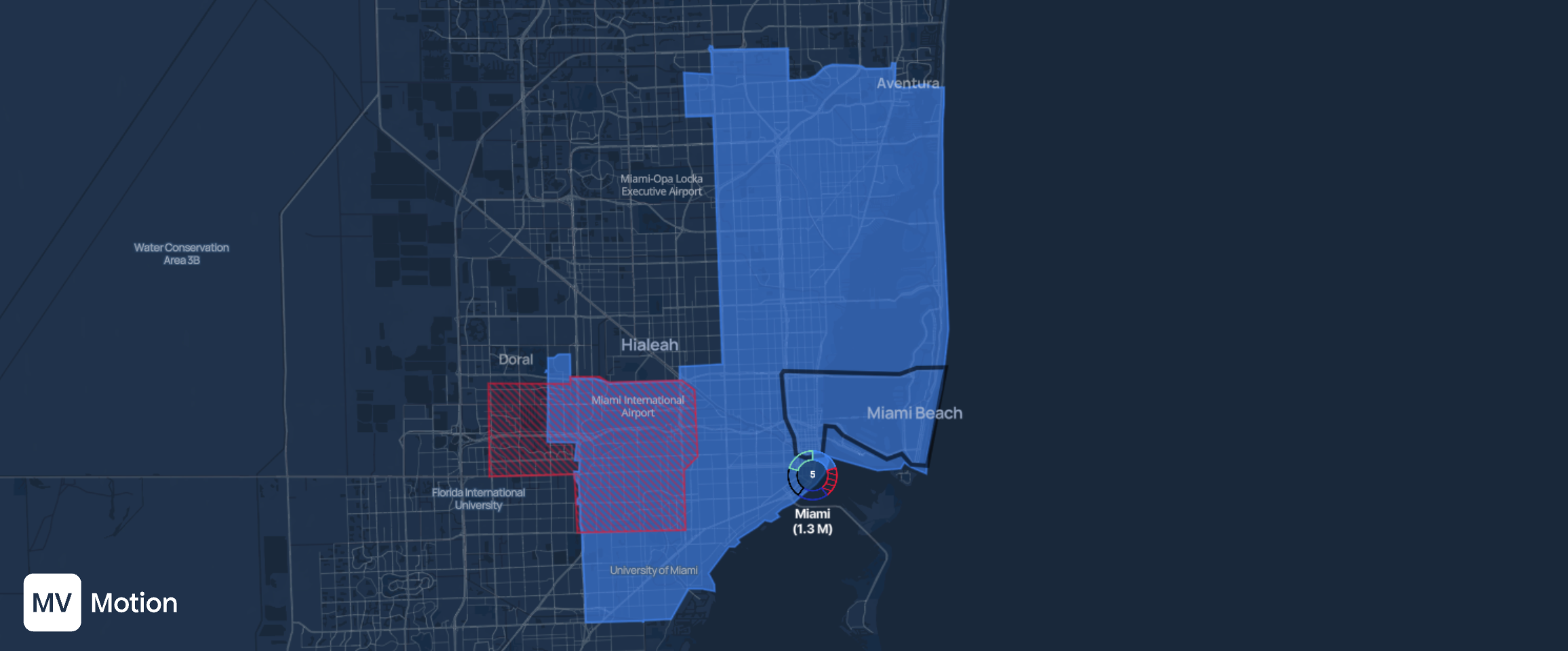

Tesla launched its robotaxi service in Miami, extending its autonomous ride-hailing network into Florida. The initial rollout is geographically limited, with a small geofence covering parts of West Miami and stretching toward Doral and Sweetwater, rather than the city’s main coastal districts. Tesla’s entry adds another competitor to Miami’s emerging robotaxi market, where Waymo already operates a substantially larger service area with several smaller companies undergoing tests.

Tesla's geofence in Miami

Source: RobotaxiMap.com

Disclaimer

This report and the information within are not investment advice or an offer to sell or a solicitation of an offer to buy any security or other financial instrument. Neither the Firm nor any person related to the Firm (“We” or “Our”) are offering, selling or buying any security to or from any person through this research report. We do not provide investment advice. You understand and agree that We do not have an investment advisory relationship with you and do not owe you any fiduciary duty. You agree that use of the research presented in this report is at your own risk and that you will do your own research and due diligence beforemaking any investment decision regarding any securities related to any issuer(s) discussed herein (“Covered Issuer”) or any other financial instruments that reference the Covered Issuer or any securities issued by the Covered Issuer. You represent that you have sufficient investment sophistication to critically assess the information, analysis and information presented in this report. You further agree that you will not communicate the contents or information in this report to any other person. This report reflects and expresses Our analysis as of the time of the report only. This report is based on generally available information, field research, inferences and deductions through Our due diligence and analytical process. To the best of Our ability and belief, all information contained herein is accurate and reliable, is not material non-public information, and has been obtained from public sources that We believe to be accurate and reliable. Further to the best of Our ability and belief, all information has been obtained from sources that are not insiders or connected persons of any Covered Issuers or who may otherwise owe a fiduciary duty, duty of confidentiality or any other duty to the Covered Issuer (directly or indirectly). However, such information is presented “as is,” without warranty of any kind, whether express or implied. With respect to the report, We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or regarding the results to be obtained fromits use. Further, this report only contains Our analysis and information. All information in the report is subject to change without notice, and We will not update or supplement this report or any of the information, analysis or information contained therein. We generally invest in broad based and sector related indexes, typically via mutual funds and exchange traded funds. As of the publication date of this report, We also have positions in Tesla, Nvidia, and other individual companies. Thus, We will realize gains if the prices of these securities appreciate. We may trade in Tesla and/or Nvidia stock, the other securities, or the indexes after this report, and such position(s) may be long, short, or neutral at any time hereafter regardless of the comments, information, or views stated in the report. We will not update this report or information to reflect changes in any positions held or any trades.